|

| By Ted Baumann |

Native-born Americans are exceptional.

By that, I mean we are unique amongst citizens of the world’s many countries.

U.S. citizenship is based on the concepts of jus sanguinis — the right of blood — and jus soli — the right of soil.

Anyone born on American soil automatically becomes a citizen. Even if their parents aren’t.

Every citizen is considered a “U.S. person.”

That’s a legal term. It simply means we are immediately subject to the U.S. tax system.

I’ll say that again …

As soon as you are born, you are technically a taxpayer.

Even though you don’t need to file until you earn an income. And, generally, no matter where in the world you reside.

Now, here’s where things diverge from the rest of the planet.

Every other country of consequence — the exceptions being Eritrea and North Korea — consider their citizens to be taxpayers when they live in their home country.

If they move to another country and establish permanent residence there, the road diverges from a typical American expat’s.

In other words, they cease to be a taxpayer … even though they continue to be a citizen.

This is known as “tax domicile.”

Let’s say you’re a citizen of Italy, and you move to Brazil. You become domiciled in Brazil for tax purposes.

Therefore, you owe taxes to Brazil, but not to Italy, even though you continue to be its citizen.

Americans, on the other hand, continue to be domiciled in the U.S. for tax purposes … even if they don’t live or earn income there anymore.

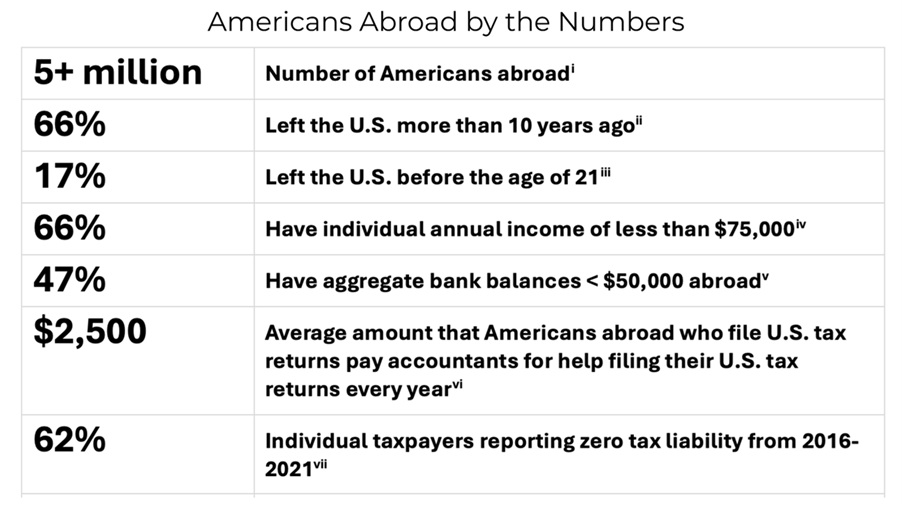

That’s a lot of revenue Uncle Sam doesn’t want to let go of, as you can see below.

Certain exemptions and credits are granted to U.S. citizens who live abroad, yes. But they’re still required to file taxes with the IRS.

I liken this to original sin, the notion that we are all born guilty in the eyes of God: Being born an American citizen means you are forever tied to the country for tax purposes.

So, when I saw this headline on Friday, it didn’t even shock me:

U.S. citizens domiciled abroad can reduce their tax obligations, however. Here are two ways:

-

They can claim a credit against their U.S. taxes for income taxes paid to a foreign government.

Let’s say you owe the IRS $25,000 in income tax on your global income. But you’ve already paid $20,000 in tax to the government of the country where you live and work. That means you only owe the IRS $5,000.

If you live in a country with higher tax rates than the U.S., you won’t owe the IRS anything.

-

They can exempt income up to a fixed amount from their U.S. taxable income.

Certain types of income are exempted from U.S. taxation.What remains is your “taxable income.”

Under the Foreign Earned Income Exclusion, or FEIE, an individual can exempt up to $126,500 of foreign-earned income from their taxable income. A couple filing jointly can exclude twice that.

For all intents and purposes, it’s as though you never earned the income. Anything above the FEIE limit is subject to U.S. tax as normal.

In addition to the FEIE, U.S. citizens living abroad may qualify for the Foreign Housing Exclusion or Deduction. That exempts or deducts up to 16% of the FEIE limit to provide for housing expenses incurred abroad.

Note that the FEIE only applies to earned income, i.e., income from current work or business activities.

It doesn’t apply to passive income like pensions, Social Security, rental income, investment income and so on.

And it only applies to income earned from work performed in a foreign country.

Bottom line, you can’t escape the U.S. government’s taxmen completely while remaining a citizen.

However, you can escape with your wealth. And I can show you how.

Tomorrow at 2 p.m. Eastern, join Nilus Mattive and me for an Emergency Wealth Conclave, where we will discuss exactly how to protect your funds from snooping government eyes …

And show you how to plant the seeds for future wealth far away from government overreach.

Best wishes,

Ted Baumann