Does the Big, Beautiful Bill Mean a ‘BBB’ for America?

|

| By Nilus Mattive |

Last week, the House passed its version of President Trump’s “big, beautiful bill.”

It’s a comprehensive piece of legislation that overhauls the U.S. tax code in several meaningful ways … proposes cuts to the country’s Medicaid and Food Stamp programs … and allocates roughly $150 billion for additional military spending on things like the construction of a new “golden dome” missile defense shield.

Make no mistake, the bill IS big. It’s about 1,000 pages long.

At least some parts of it are beautiful, too … though which parts depend on the eye of the beholder.

If you rely on tips or overtime pay, you’ll like the provision that exempts such income from federal taxation.

If you live in a high-tax state like I do, you’ll like the big expansion of the SALT deduction.

If you’re shopping for a new car or all-terrain vehicle, you’ll like the idea that interest on associated loans could become tax deductible.

There’s pretty much something for everyone in the big, beautiful bill.

That’s also the problem.

Because there’s no way the big, beautiful bill won’t also make the U.S. worse off financially.

Most estimates peg the specific number somewhere between $3 trillion and $4 trillion — adding another 10% to America’s existing $36 trillion national debt.

This is precisely why Representative Thomas Massie from Kentucky was one of two Republicans to break from the party and vote “No” on the BBB. As he explained it …

“While I love many things in the bill, promising someone else will cut spending in the future does not cut spending. Deficits do matter and this bill grows them now. The only Congress we can control is the one we’re in. Consequently, I cannot support this big deficit plan.”

Is Massie just grandstanding, as many claim?

I don’t think so.

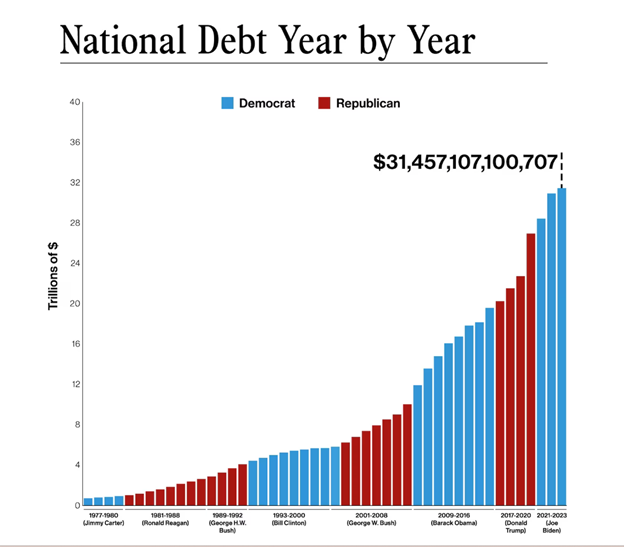

Here’s a long-term chart of the U.S. national debt through 2023 …

You can see that it rose under every single President, regardless of party.

And again, after Joe Biden’s final year in office, it is trillions worse than what that chart depicts.

At this point, the U.S. government is now spending more on interest payments than national defense!

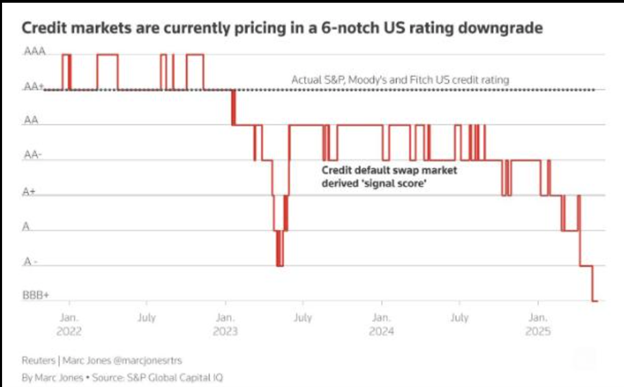

This ever-worsening financial picture is precisely why Moody’s finally joined other major credit ratings agencies and downgraded the U.S. from a top-level “AAA” rating on May 16.

This could be the tip of iceberg.

In fact, my friend and colleague Sean Brodrick recently passed along this chart that shows credit markets are currently pricing in the possibility of the U.S. seeing its rating drop all the way down to BBB … which is barely “investment grade.”

It’s hard to ignore the possible irony of the Big Beautiful Bill resulting in U.S. bonds getting slapped with a BBB rating.

And while they have been generally complacent about skyrocketing government debt over the last several decades, bond markets are no longer ignoring the situation at all.

Yields on 30-year Treasury bonds are now sitting at their highest level in roughly 15 years.

That means the government’s lenders are demanding more interest to take on the risk of loaning money to Uncle Sam. In fact, as Bloomberg just reported …

“The U.S. 10-year term premium — or the extra return investors demand to own longer-term debt instead of a series of shorter ones — has climbed to near 1%, a level last seen in 2014. It’s a measure of how jittery investors are about plans to raise the scale of future borrowing.”

Hey, maybe this is as far as it goes.

Maybe tariffs and/or economic growth will start reversing decades of government largesse and chronic malfeasance.

But I don’t recommend betting everything on that.

How to Invest for Darker Dollar Days

We’re hearing a lot more about the “Sell America” trade … the idea that foreign investors are dumping U.S. government bonds … pulling money out of U.S. stocks … and moving away from anything else denominated in U.S. dollars as well.

I’m not suggesting you do that at all.

In fact, I still have hundreds of thousands of dollars of my own money parked in U.S. government bonds despite all the bad stuff I just outlined.

I’m simply suggesting you diversify beyond traditional financial assets and get more protection from the possibility that the U.S. dollar experiences a more serious decline from here.

You might even consider taking extra steps to move some of your assets outside the U.S. financial system entirely.

How do you do it exactly?

Just watch this video and find out.

I put it together with my friend and colleague Ted Baumann, an expert in offshoring strategies.

As you’ll see, we cover a whole range of ideas you can start implementing right away — including details on which particular assets provide the best combination of “off-grid” protection and massive profit potential.

In fact, this week, I’m getting a small group of readers first-mover advantage on an extremely rare, private asset.

Only 171 of these exist … and it’s not a gold coin or a crypto or even a bottle of wine.

But the last eight times these assets were resold, they brought back an average of 965 times investors’ money.

So, if you’re interested, you need to watch this video right now because we’ll be pulling it offline by midnight tomorrow.

Best wishes,

Nilus Mattive