How Neoclouds Will Disrupt a $395 Billion Market

|

| By Michael A. Robinson |

One of the great things about tech is that there’s always a new company rewriting the rules.

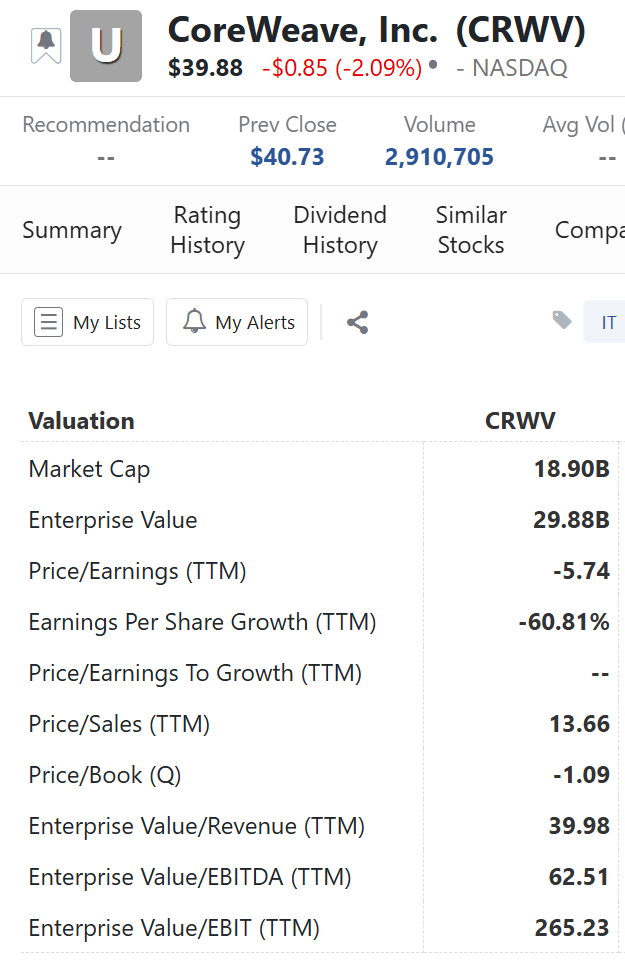

That’s exactly what we’re seeing with CoreWeave (CRWV) — a fast-rising force in a disruptive new field known as “neoclouds.”

If you haven’t heard the term before, you’re not alone. Neoclouds are flying under the radar of Wall Street and Big Media alike. But they won’t stay secret for long.

These platforms represent a foundational shift in how the world will run artificial intelligence.

Unlike traditional cloud services, neoclouds are built from the ground up for AI.

They deliver extreme performance for training massive models, crunching real-time data and powering next-gen breakthroughs from self-driving cars to personalized medicine.

It’s a market set to explode — worth an estimated $395 billion by 2030.

CoreWeave is already leading the charge.

But here’s the catch: As a brand-new IPO, the stock is just too volatile right now to recommend.

That’s OK. Because I’ve found the company that helped launch CoreWeave into orbit … and it’s on pace to double its earnings this year — and again the next.

Let’s dive in …

The Strategic Powerhouse

Behind the Neocloud Revolution

So, what exactly are neoclouds?

Think of them as the next phase of cloud computing — designed from day one for AI.

While traditional cloud providers like Amazon Web Services or Microsoft Azure serve a wide range of generic business needs, neoclouds are laser-focused on one thing — high-performance AI workloads.

These platforms use purpose-built hardware like advanced GPUs, AI accelerators and ultra-fast networking to handle tasks that legacy clouds simply weren’t built for.

That includes training massive generative models like ChatGPT, simulating real-world environments for autonomous vehicles or processing real-time insights in financial markets.

In other words, this is the backbone infrastructure for the global AI economy.

And the demand is relentless.

Training today’s most powerful AI models can cost millions. Running them? Even more.

That’s why companies — startups and giants alike — are turning to neocloud providers to “rent” their way into AI dominance.

Which brings us back to CoreWeave.

It’s the poster child of this movement: A fast-scaling platform purpose-built for AI, offering clients access to the same kind of compute firepower used by the biggest names in tech.

The company started as a niche GPU operation — but now it’s dominating the high-performance rental market for AI infrastructure.

That’s exactly why it just went public.

And while the headlines around the IPO are exciting, let me be crystal clear: This isn’t the time to jump in.

Early IPOs are notoriously volatile — especially in choppy markets like these. Even great companies can whip investors around in the early months.

That’s why CoreWeave is firmly on our watchlist, not our buy list … yet.

But here’s the good news …

You don’t have to wait on CoreWeave to profit from this $395 billion trend.

Because the most powerful neocloud player in the world isn’t a startup — it’s a name you already know.

And thanks to a recent pullback, it’s started to trade at what I consider a strategic discount …

The One Stock Already

Cashing in on the Neocloud Boom

That company?

Nvidia (NVDA), of course.

Yes, the same Nvidia known for its dominance in the GPU space.

But this isn’t just about chips anymore.

Nvidia is now the strategic engine driving the entire neocloud ecosystem forward.

It’s not only supplying the GPUs that power AI platforms like CoreWeave — it’s investing in them directly.

In fact, Nvidia helped fund CoreWeave’s growth through a major investment round in 2023. That $221 million Series B wasn’t just a vote of confidence — it was a tactical move to embed Nvidia deeper into the infrastructure of next-gen AI.

CoreWeave, in turn, built its entire business around Nvidia GPUs.

So, every time an AI firm rents compute time from CoreWeave, Nvidia benefits — both from chip sales and from growing demand for AI-optimized infrastructure.

Now add in Nvidia’s own growing presence in cloud-scale AI rentals … and you start to see the full picture:

Nvidia Remains Critical to AI’s Build-Out

And Nvidia isn’t slowing down. The company recently unveiled its next-generation AI chip — Blackwell — which offers up to 4x the performance of its predecessor — the Hopper H100 — in generative AI inference tasks.

This leap in capability has led to unprecedented demand, with Nvidia reporting $11 billion in revenue from Blackwell chips in Q4 alone — the fastest product ramp in the company’s history.

In fact, last year, the firm said its Blackwell GPUs were already sold out for the next 12 months.

Talk about a powerful one-two punch: Last month, the firm said that an updated version, new Blackwell Ultra offers 1.5 times the performance of Blackwell.

That’s why the pullback in NVDA during the Tariff Tantrums should be seen not as a red flag … but as an opening door.

This is a company that just grew earnings per share by 71% year over year.

At that pace, Nvidia is on track to double its earnings this year —and again the next.

It’s not hype. It’s math.

And for long-haul investors, that’s exactly the kind of momentum you want to own.

In the short term, I also have to note that Nvidia announced it was going to take a $5.5 billion charge to export its H20 GPUs to China and other countries.

So, you may be able to get in at an even lower price if you are hoping to ride that momentum.

Remember, in this market, you can be aggressive in price by putting in a limit order at a further discount from the current price as a margin of safety.

Best,

Michael A. Robinson

P.S. We have our own AI working behind the scenes here at Weiss Ratings.

And on Tuesday, April 22, at 2 p.m. Eastern, Dr. Martin Weiss will show you how it beats the S&P 500 by 94-to-1 in ANY market. Grab your VIP seat here.