|

| By Nilus Mattive |

It’s hard to believe, but I started my formal career on Wall Street 25 years ago. And I was lucky enough to work with some very smart “old school” mentors.

They taught me all about value investing, the importance of dividends, avoiding hype and the merits of a slow-and-steady approach to the financial markets.

I still rely on their lessons to this very day.

But I’m no longer JUST a dividend stock guy. Nor even a pure income investor trying to find an optimal balance between stocks and bonds.

It is still absolutely true that asset allocation — i.e., how you diversify across the big investment categories — is the biggest determining factor in how your overall portfolio performs.

However, the traditional notion of diversification that Wall Street pushes on individual investors is woefully outdated.

Take a look at any “target retirement date” fund and you’ll see what I mean.

It will typically consist of various stock and bond funds. No gold. No silver. No private equity. No real estate. No inverse market hedges. And definitely no crypto.

The Vanguard Target Retirement 2035 Fund (VTTHX) is a great example.

Meanwhile, you’ll get an even worse version if you go to many financial advisers.

They’ll also look at your age, ask about your goals and come up with a simple mix of stocks and bonds — the so-called 60/40 model.

Then, in many cases, they’ll use their own company’s mutual funds or exchange-traded funds to fulfill that mix just like a target date mutual fund.

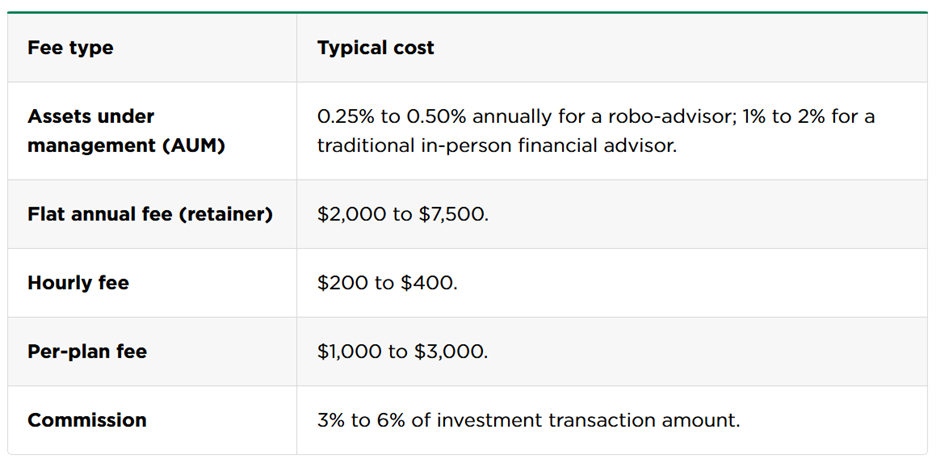

However, on top of the fees you pay for the funds, they’ll also pocket a percentage point or two of your assets every single year just for the privilege of pushing the buttons on your behalf and checking in with you every couple of months.

So, you have to make up the lost ground in fees just to break even.

The average adviser charges somewhere between 0.5% and 2% a year. Unless they’re helping you beat the markets by that amount or more, you’re losing money.

And let’s be real: While some advisers are worth their fees, most are not helping people beat the markets by two percentage points a year.

That’s especially true if they’re ultimately putting their clients into index funds that are simply designed to MATCH the market’s performance!

But no matter what, you are not getting TRUE diversification.

Fifty years ago, a 60/40 portfolio made a lot of sense.

Most Americans didn’t even own stocks at all and only the ultrarich were able to invest in things like private companies or fine art.

So, holding 60% of your money in equities and 40% of your money in fixed-income — or some other similar percentage mix — was a solid plan.

Today, it makes less sense for two reasons.

First, stocks and bonds have moved in tandem more often in the modern Fed-manipulated era, especially during times of heightened inflation expectations.

Heck, we’ve seen both stocks and bonds move lower this month!

Second, and more importantly, everyday investors now have cheap, easy and liquid access to just about any type of asset you can think of … including things like cryptocurrencies, which didn’t even exist 20 years ago!

Many of these assets have low correlations to each other and stocks or bonds.

This is a crucial point, and the big reason my readers’ Safe Money Report Portfolio has been powering higher over the past few years, even though I’ve been extremely bearish on richly valued stocks like the so-called “Magnificent Seven.”

How My Approach Has Evolved

After 25 Years as a Professional Analyst

Stocks still make up the bulk of my active recommendations in Safe Money Report. I don’t expect that to ever change.

Owning solid companies — especially ones that pay healthy and rising dividends — is THE time-tested path to growing wealth consistently through thick and thin. My mentors were 100% right about that.

Likewise, I think it makes sense to have some of your money allocated to the fixed-income markets as well. That’s especially true right now since a brutal bond bear market has been keeping prices down and yields up.

But I have two additional goals for the recommendations I make.

Goal No. 1: I want to make sure members are adequately diversified across ALL asset classes.

This is pretty simple, and I already covered it above. But the aim is making sure I give my readers ideas in stocks, bonds, real estate, precious metals and alternative asset categories as well.

Goal No. 2. I also want to make sure they are adequately diversified within asset classes.

I certainly do a lot of research to identify stocks with big catalysts. I also have a solid team helping me, along with the power of the Weiss Ratings.

However, Safe Money Report does not have a niche focus on tech stocks, biotechnology, resources or anything else.

Instead, I want to continually give you new stock ideas in DIFFERENT market sectors and industries. That way, you don’t get crushed if an entire area of the markets turns cold.

Bottom line?

I aim to operate more like a macroeconomic hedge fund — looking at all the big-picture forces in place … considering all the asset classes available … and then making the very best recommendations at the very best times to keep readers’ money growing no matter what happens next.

And the most important tool I use is now available to you!

We recently upgraded our website to offer more data that is even easier to parse to help you diversify your portfolio.

We added advanced screeners and alerts that will notify you when stocks first become “buys” and “sells.”

But to access it, you need to check out this presentation.

Best wishes,

Nilus Mattive